How To Read Your 2026 Medicare Annual Notice Of Change Before It Costs You

Most Medicare mistakes do not begin with a dramatic denial letter. They begin quietly, in early fall, when a thick envelope arrives from a plan a beneficiary has had for years. The cover may look routine. The language may feel repetitive. For many people, the instinct is to set it aside because last year’s plan worked well enough.

That is exactly where 2026 Medicare planning can go wrong. The Annual Notice of Change is not a courtesy mailing. It is the plan’s formal warning that the rules may be different in January. Medicare explains that this notice can include changes in coverage, costs, provider networks, service area, and other plan details that take effect in the new year . For a beneficiary taking several medications, seeing specialists, using a preferred pharmacy, or relying on a Medicare Advantage network, those changes can alter the real value of a plan even when the premium barely moves.

Why The Annual Notice Of Change Matters More In 2026

The 2026 Medicare year is unusual because several moving parts are converging at once. Prescription drug costs are capped at $2,100 in annual out of pocket spending for covered Part D drugs, and once that cap is reached, a beneficiary owes no copayment or coinsurance for covered Part D drugs for the rest of the calendar year . That sounds simple, but the cap does not mean every drug is covered, every pharmacy prices the same, or every plan treats a medication the same way.

Consider a retiree who takes a brand name heart medication, an inhaler, and a diabetes drug. In 2025, she may have chosen her plan because the premium was modest and her local pharmacy was preferred. In 2026, the same plan could still advertise an attractive premium, but one medication may move to a higher tier, prior authorization may be added, or the pharmacy she has used for a decade may no longer receive preferred cost sharing. The $2,100 cap can protect against unlimited covered Part D spending, but it does not protect against choosing a plan that poorly matches the drugs, pharmacies, and access rules she actually needs.

The Parts Most People Read Last Are Often The Most Important

Many beneficiaries look first at the monthly premium. That is understandable, but it is rarely enough. Medicare notes that drug costs vary based on the prescriptions a person takes, whether those prescriptions are on the formulary, what tier each drug is assigned to, which benefit phase applies, which pharmacy is used, and whether the person receives Extra Help . In broker language, that means the same plan can be inexpensive for one neighbor and costly for another, even if both live on the same street.

The same is true for Medicare Advantage plans. A plan may still include dental, vision, hearing, transportation, fitness, or an over the counter allowance, but the medical core of the plan is where the financial risk often lives. Medicare explains that Medicare Advantage out of pocket costs can depend on the plan premium, deductibles, copayments, coinsurance, network status, use of out of network providers, extra benefits, and the plan’s yearly limit for Part A and Part B covered services . A beneficiary who focuses only on the extras can miss a higher specialist copay, a changed hospital system, or a tighter referral rule.

A Broker Level Reading Starts With Real Life, Not The Brochure

The right way to read an Annual Notice of Change is to begin with the person’s actual care pattern. A healthy 66 year old who sees a primary care doctor twice a year has a very different risk profile than a 74 year old with rheumatoid arthritis, an oncologist, three brand name medications, and a preferred specialist across county lines. The plan document is not the starting point. The person is.

A practical review should ask one central question: if January 1 arrived tomorrow and you had a normal medical year, would this plan still behave the way you expect? That means checking the primary doctor, specialists, hospitals, imaging locations, durable medical equipment suppliers, pharmacies, and each prescription by exact name, dosage, quantity, and frequency. It also means looking for quiet wording changes, such as new authorization requirements, tier changes, pharmacy network adjustments, or a service area change. Medicare Advantage plans may require approval before covering certain services or supplies, while Original Medicare generally does not require prior authorization for most covered services and supplies . That difference can be decisive for someone who receives recurring treatment.

The 2026 Drug Cap Does Not Replace Plan Comparison

The $2,100 Part D cap is one of the most important consumer protections in 2026, but it should not create false confidence. It applies to covered drugs under the plan. If a medication is not on the formulary, is subject to an exception process, or has access restrictions that delay therapy, the beneficiary’s experience can still be frustrating and expensive in ways that are not obvious from a headline.

Medicare also points out that drug plans may have deductibles, although some plans do not, and some drugs may be covered before the deductible depending on the plan’s tier design . That creates a timing issue. Two plans may both lead a high cost drug user toward the same annual cap, but one plan may front load costs early in the year while another may smooth them differently. The Medicare Prescription Payment Plan can help spread covered drug out of pocket costs across the calendar year, but Medicare is clear that it does not save money or lower drug costs . For retirees on fixed income, cash flow can matter nearly as much as the annual total.

The Calendar Is Part Of The Strategy

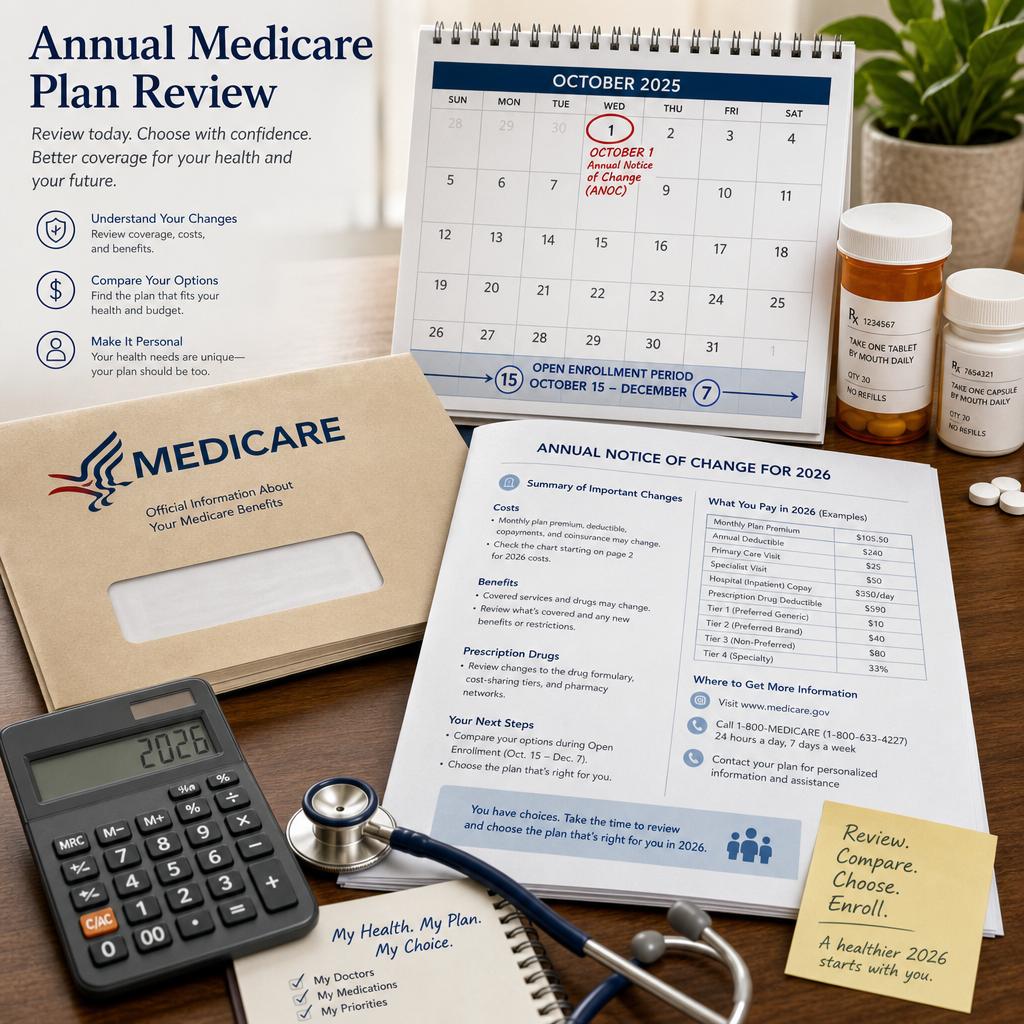

The fall review window is not a vague suggestion. Medicare says October 1, 2025 is when beneficiaries can start comparing their current Medicare health or drug coverage with 2026 options, and October 15 through December 7, 2025 is the Open Enrollment Period to join, switch, or drop a Medicare Advantage Plan or Medicare drug plan for 2026 . Waiting until Thanksgiving or early December compresses the work into the same season when pharmacies are busy, doctors’ offices are hard to reach, and plan call centers may be overwhelmed.

There is another subtle issue: some beneficiaries assume that because they do not want to change plans, they do not need to review anything. Medicare itself advises people to review their Medicare health and drug coverage each year to make sure it still meets their needs . Staying put can be the right decision, but it should be an informed decision, not an accidental one.

When Staying With The Same Plan Is The Right Move

A careful review does not always end in a plan change. Sometimes the best recommendation is to keep the current plan because the doctors remain in network, the hospital system is stable, the medications are still covered favorably, and the total cost exposure is reasonable. That kind of confirmation has value. It prevents a beneficiary from being lured by a richer looking extra benefit while unknowingly giving up access to a trusted specialist or creating drug friction.

The danger is that Medicare marketing often encourages shoppers to compare visible perks while the Annual Notice of Change contains the less glamorous facts that determine whether care will be smooth. A $0 premium Medicare Advantage plan may still require the Part B premium, may have copays for frequent services, and may limit non-emergency care to network rules. Medicare notes that some Medicare Advantage plans have $0 premiums, but beneficiaries may still pay the Part B premium and possibly an additional plan premium depending on the plan . The premium is only one line in a much larger financial contract.

Professional Review Turns Fine Print Into Peace Of Mind

The Annual Notice of Change is one of the clearest examples of why Medicare is not a one time enrollment decision. It is a living arrangement between your health needs, your doctors, your medications, your pharmacy habits, and the rules your plan adopts for the new year. In 2026, the new Part D cap, changing plan designs, and evolving Medicare Advantage networks make that review even more important.

Vista Mutual Insurance Services helps clients translate these documents into real world consequences. The goal is not to chase every new benefit or react to every premium change. The goal is to protect access, anticipate costs, and make a decision that still feels sound when you are sitting in a doctor’s office, standing at the pharmacy counter, or opening a bill in February. If you want a professional review before the 2026 plan year begins, Schedule your 2026 Medicare consultation with the Vista Mutual team.