Medicare Advantage Organization Determinations In 2026

A Medicare Advantage plan can look simple on the surface. A familiar doctor appears in the directory, a specialist says a procedure is routine, and the plan brochure uses reassuring language about covered benefits. Then, in the middle of a serious diagnosis or scheduled surgery, the beneficiary discovers the real question was never whether Medicare covers the service in general. The question was whether this specific plan would cover this specific service, from this specific provider, under these specific rules.

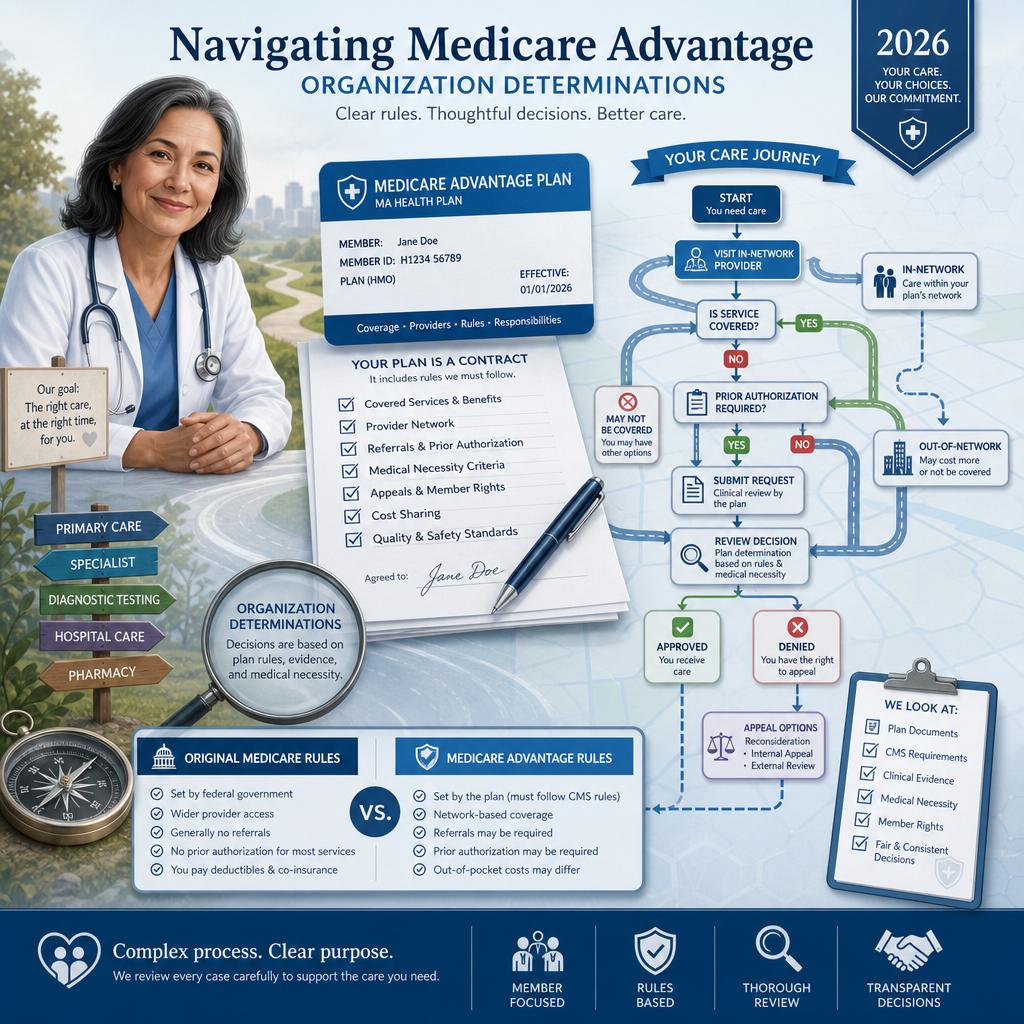

That is why organization determinations deserve far more attention in 2026. Medicare explains that Medicare Advantage plans are another way to receive Part A and Part B benefits through private companies approved by Medicare, and these plans may require beneficiaries to use network providers, obtain referrals, or receive approval before certain services or drugs are covered . The practical lesson is direct: the plan card in your wallet is not just an insurance card. It is a contract with rules, decision points, and appeal rights.

The Coverage Decision That Should Happen Before The Bill Exists

An organization determination is a formal coverage decision from a Medicare Advantage plan. It can address whether a service, drug, or supply is covered, whether it is medically necessary under the plan rules, and how much the beneficiary may have to pay. Medicare states that you, your representative, or your doctor can ask the plan for this decision, either orally or in writing, and that sometimes this process is tied to prior authorization for the plan to cover the service, drug, or supply .

For a healthy beneficiary who sees a primary care physician twice a year, this may sound procedural. For someone facing chemotherapy, advanced imaging, a skilled nursing transition, home medical equipment, or a specialist referral outside the usual network, it can be financially decisive. A verbal reassurance from a scheduler is not the same as a plan decision. A doctor saying, “Medicare covers this,” may be true under Original Medicare, yet incomplete under Medicare Advantage. The beneficiary needs to know whether the plan has approved the pathway before the service is rendered.

Why 2026 Makes This More Important

The Medicare landscape in 2026 gives beneficiaries more reasons to look beyond premiums. Medicare Advantage plans may have different out-of-pocket costs for certain services, may require network use, may require referrals for specialists, and may require prior authorization for certain services or supplies . The same official comparison also emphasizes a major structural difference: Original Medicare has no yearly out-of-pocket limit unless a person has other coverage such as Medigap, Medicaid, employer, retiree, or union coverage, while Medicare Advantage plans do set annual limits for covered Part A and Part B services .

That annual limit can be valuable, but it does not eliminate the need to follow plan rules. A service denied as not covered, not authorized, out of network, or not medically necessary may not move neatly into the protection a beneficiary expected. In 2026, the sophistication of the decision is not simply choosing between a low premium and a higher premium. It is understanding how the plan controls access, how the provider network functions, and where a written determination can prevent a coverage dispute from becoming a medical and financial crisis.

A Real World Scenario Beneficiaries Often Miss

Consider a retiree named Elaine who joined a Medicare Advantage PPO because her cardiologist was listed as in network and the plan included drug coverage. In February 2026, she develops worsening shortness of breath. Her cardiologist recommends an outpatient procedure at a hospital system that the cardiology group uses frequently. Elaine assumes that because the physician is in network, the facility and anesthesia group will be handled the same way.

That assumption is where Medicare Advantage problems often begin. Medicare notes that costs in a Medicare Advantage plan can depend on whether services come from network providers, whether providers contract with the plan, whether additional deductibles apply, and whether the plan requires approval before covering a service or supply . Elaine does not need a brochure at that moment. She needs a plan-level answer that confirms coverage, provider status, authorization requirements, and likely cost sharing before the procedure is performed.

The Difference Between Covered By Medicare And Covered By Your Plan

Original Medicare and Medicare Advantage begin with the same broad foundation, but they do not operate the same way. Original Medicare generally allows beneficiaries to use any Medicare-enrolled provider who accepts Medicare patients anywhere in the United States, while Medicare Advantage beneficiaries may need to use providers in the plan network and service area for non-emergency care . That distinction can be especially important for people who split time between states, receive care from academic medical centers, or depend on a narrow group of specialists.

The phrase “covered by Medicare” can be misleading when used casually. A knee replacement, infusion therapy, diagnostic scan, or durable medical equipment item may fall within Medicare-covered categories, but the Medicare Advantage plan may still require a contracted supplier, a specific site of care, documentation of medical necessity, or prior approval. If the beneficiary waits until after the claim is denied, the appeal process may still exist, but the leverage and timing are different. A pre-service organization determination can turn ambiguity into a documented plan position.

The Drug Coverage Connection In 2026

Organization determinations also matter because Medicare Advantage often includes Part D drug coverage. Medicare confirms that most Medicare Advantage plans include Medicare drug coverage, and drug costs can vary based on formularies, tiers, pharmacy choice, benefit phase, and whether a beneficiary qualifies for Extra Help . For 2026, the annual out-of-pocket cost cap for covered Part D drugs is $2,100, after which the beneficiary does not pay a copayment or coinsurance for covered Part D drugs for the rest of the calendar year .

That cap is meaningful, but it applies to covered Part D drugs. It does not automatically solve formulary exclusions, tier placement issues, pharmacy network differences, or medical benefit versus pharmacy benefit confusion. A drug given in a physician office may be handled differently from a drug picked up at a pharmacy. A plan may include a medication on its formulary but still apply utilization management. The beneficiary who asks questions early is not being difficult. They are protecting access to therapy.

What A Careful 2026 Review Should Ask

Before a high-cost service is scheduled, a careful beneficiary should ask the Medicare Advantage plan whether the provider, facility, and supplier are in network, whether prior authorization is required, whether a referral is needed, whether the plan will issue an organization determination, and what cost sharing is expected if the service is approved. This is the one list worth keeping because these questions are not administrative trivia. They are the difference between confident planning and a denial letter arriving after the fact.

The strongest Medicare planning in 2026 is not limited to comparing monthly premiums. It examines how the plan behaves when care becomes complex. A plan with attractive extras may still be a poor fit if a key oncology center, orthopedic group, hospital system, neurologist, infusion site, or durable medical equipment supplier is difficult to access. Conversely, a plan with modest extras may be excellent for someone whose doctors, prescriptions, and likely care settings align cleanly with its rules.

Medicare decisions are personal, but they are not simple. The right guidance can help you read beyond marketing language, identify where a written coverage decision is prudent, and choose coverage that fits the way you actually receive care. For peace of mind before the 2026 plan year, Consult with the Vista Mutual team and make sure your Medicare strategy is built around both benefits and the rules that control them.