Medicare Claim Audits And Summary Notices In 2026

Most Medicare mistakes do not begin with a dramatic denial letter. They often begin quietly, with a code on a statement, a provider who did not accept assignment, a pharmacy transaction that did not count the way someone expected, or a bill that looks official enough to pay without question. In 2026, as Medicare Advantage networks, Part D drug cost protections, and digital Medicare records become more central to everyday coverage, beneficiaries need to treat claim review as part of their health care routine, not as paperwork to ignore.

Consider a retired couple who did everything that sounded responsible. They chose a plan during Open Enrollment, confirmed their primary doctor, and kept their prescription list updated. Then, in March, a specialist visit led to an unexpected bill. The appointment was covered, but the way the provider contracted with Medicare changed the beneficiary responsibility. That is the kind of gap a polished brochure rarely explains, and it is where professional Medicare guidance becomes more than plan shopping.

Why Your Medicare Summary Notice Is Not Just A Receipt

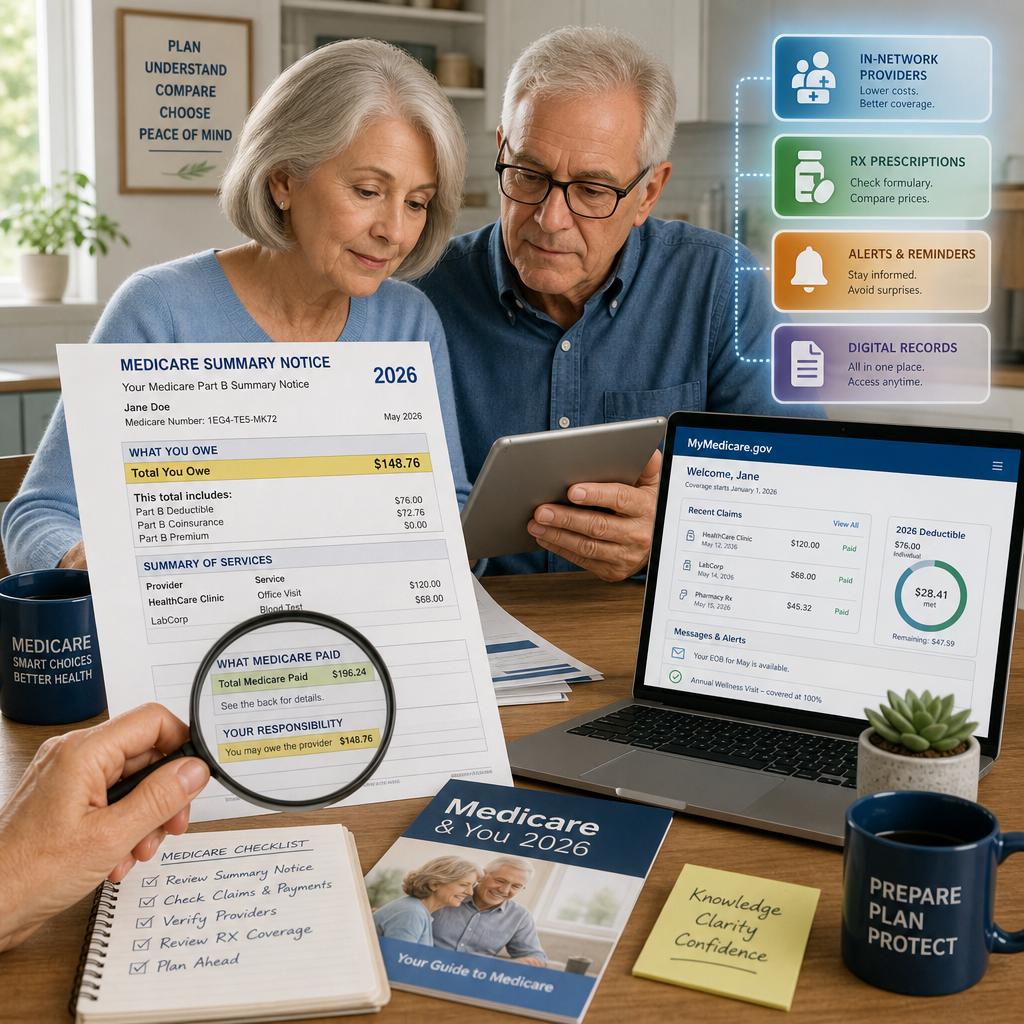

For people with Original Medicare, the Medicare Summary Notice is one of the most important documents in the system. It lists services billed to Medicare, but Medicare is clear that the MSN is not a bill fileciteturn0file4. That distinction matters because many beneficiaries see a dollar amount, assume payment is due, and act before understanding whether Medicare approved the service, what Medicare paid, and whether a supplemental policy, Medicaid, employer retiree coverage, or another payer still needs to process the claim.

The MSN is also a fraud detection tool. Medicare specifically encourages beneficiaries to review Medicare Summary Notices, receipts, and statements for errors or services they did not receive, and to report suspected misuse of a Medicare Number fileciteturn0file1. In practical terms, this means a beneficiary should not wait until a collection notice arrives to ask whether a claim was coded correctly. A physical therapy visit billed on the wrong date, a durable medical equipment charge for supplies never received, or a duplicate outpatient service can create confusion that is far easier to correct early.

The Assignment Question That Changes The Bill

One of the most misunderstood Medicare billing concepts is assignment. In Medicare language, assignment means the doctor, provider, or supplier agrees to be paid directly by Medicare, accepts the Medicare approved amount as payment in full, and will not bill the beneficiary for more than the deductible and coinsurance fileciteturn0file8. That sounds technical, but for a household budget it is very concrete. The same covered service can feel financially different depending on whether the provider accepts assignment, participates in Medicare, or has opted out entirely.

The risk is not always obvious at the front desk. Medicare notes that providers who do not accept assignment may be able to charge more than the Medicare approved amount, often up to 15 percent above that amount under the limiting charge rules fileciteturn0file18. A beneficiary who is focused only on whether a physician “takes Medicare” may miss the more precise question, which is whether the provider accepts assignment for the service being scheduled. That is why sophisticated Medicare planning includes provider billing behavior, not just premium comparisons.

Medicare Advantage Creates A Different Paper Trail

Medicare Advantage members usually do not receive claims in the same way as people with Original Medicare, but they have a different responsibility: understanding the plan’s rules before care occurs. Medicare Advantage plans must cover medically necessary services that Original Medicare covers, but beneficiaries may need to use network providers, obtain referrals, or get prior authorization before certain services or supplies are covered fileciteturn0file6. A service can be medically necessary and still become financially painful if the plan’s administrative path was not followed.

This is where the organization determination becomes a powerful planning tool. Medicare explains that a beneficiary, representative, or doctor can ask a Medicare Advantage plan in advance whether it will cover a service, drug, or supply and how much the beneficiary will pay fileciteturn0file9. In real life, that means a knee injection, home health order, imaging study, outpatient procedure, or specialty medication should not always be approached with a casual “they probably cover it.” The better question is whether the plan has confirmed coverage under its own rules, in writing when the stakes are high.

The 2026 Drug Cap Does Not Eliminate The Need To Track Claims

The 2026 Part D out of pocket cap is an important protection. Medicare states that yearly out of pocket costs for drugs covered by a Part D plan are capped at $2,100 in 2026, after which the beneficiary pays no copayment or coinsurance for covered Part D drugs for the rest of the calendar year fileciteturn0file5. That is welcome news for people taking expensive medications, but it does not mean every pharmacy charge automatically behaves the way a beneficiary expects.

The cap applies to covered Part D drugs, which makes formulary status, tier placement, pharmacy choice, and benefit phase tracking essential. Medicare notes that actual drug costs can vary based on whether a prescription is on the plan’s formulary, what tier it is in, which pharmacy is used, and whether the beneficiary receives Extra Help fileciteturn0file13. A drug purchased outside the plan, filled at a nonpreferred pharmacy, or affected by a coverage exception issue may not produce the same result as a beneficiary expected when reading a headline about the $2,100 cap.

A Practical 2026 Claim Review Habit

A strong claim review habit does not require becoming a Medicare technician. It requires disciplined attention at the right moments. When a new provider is involved, when a medication changes, when a plan year begins, or when a bill arrives that feels unfamiliar, the beneficiary should slow down before paying. The first step is not confrontation. It is verification.

For a cleaner review, beneficiaries should ask three questions before assuming a bill is correct:

- Did Medicare or the Medicare Advantage plan actually process this service or drug?

- Was the provider in the correct billing relationship with Medicare or the plan?

- Does the amount match the plan documents, MSN, Explanation of Benefits, or organization determination?

These questions sound simple, but they often reveal the hidden problem. A provider may have billed the wrong insurer first. A plan may have denied a service because prior authorization was missing. A pharmacy may have applied a price outside the expected preferred network arrangement. A supplemental policy may not have received the claim yet. The beneficiary who pays immediately may later need to unwind the mistake, while the beneficiary who verifies first has more leverage and clearer documentation.

Why Professional Guidance Matters More In 2026

The central Medicare decision in 2026 is not merely Original Medicare versus Medicare Advantage, or one drug plan versus another. It is whether the total system around the beneficiary works under real medical conditions. Original Medicare generally allows access to any Medicare enrolled doctor or hospital that accepts Medicare patients anywhere in the United States, while Medicare Advantage may require use of a plan network and service area for nonemergency care fileciteturn0file6. That difference affects claims, referrals, appeals, pharmacy access, travel, and specialist coordination.

Vista Mutual Insurance Services evaluates Medicare choices through that broader lens. The right plan is not always the one with the lowest premium, the largest dental allowance, or the most attractive advertisement. It is the plan that fits the beneficiary’s doctors, prescriptions, risk tolerance, travel patterns, financial exposure, and ability to navigate the paperwork that follows care.

In 2026, peace of mind will belong to beneficiaries who do not simply enroll, but understand how their coverage behaves after enrollment. A careful review of claims, notices, provider status, and drug cost tracking can prevent small administrative issues from becoming expensive surprises. If you want help evaluating your Medicare Advantage, Supplement, or Part D options with the level of detail these decisions deserve, Schedule your 2026 Medicare consultation with the Vista Mutual team.