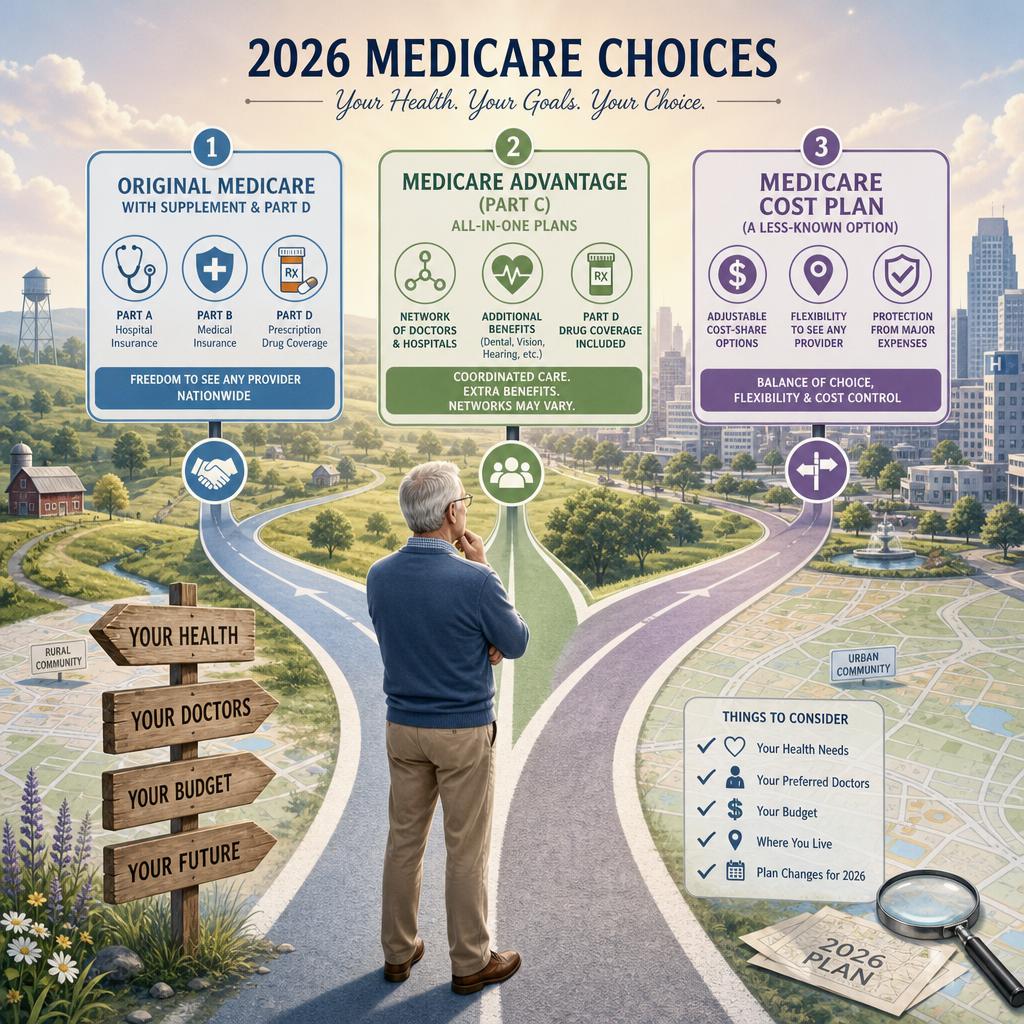

Medicare Cost Plans And The 2026 Coverage Middle Ground

A retiree comparing 2026 Medicare choices may assume there are only two practical paths: Original Medicare with a Supplement and Part D, or a Medicare Advantage plan with a network and bundled benefits. That is usually the right framework. Yet in certain parts of the country, there is a third option that can quietly change the analysis: the Medicare Cost Plan.

Cost Plans do not get the same advertising attention as Medicare Advantage, and many beneficiaries have never heard the term until it appears in a local plan comparison. That lack of familiarity is exactly why the decision deserves professional review. A Cost Plan can feel flexible on paper, but the value depends on where you live, which doctors you use, whether you have Part A, and how your prescriptions are handled in 2026.

The Medicare Option That Does Not Fit Neatly In The Box

Medicare describes Cost Plans as a type of Medicare health plan available only in certain limited areas of the country. Unlike standard Medicare Advantage enrollment, a Cost Plan may allow someone to join even if they only have Part B, and if the beneficiary has both Part A and Part B, services from a non-network provider can be covered by Original Medicare, with the beneficiary responsible for the applicable Part A and Part B deductibles and coinsurance . That one sentence contains the appeal and the trap.

The appeal is obvious for someone who likes a local plan's care coordination but does not want to feel entirely boxed into a network. Imagine a beneficiary in a rural county who sees most physicians through a regional health system but occasionally travels to a larger academic medical center. A Cost Plan may appear to offer a more forgiving structure than a narrow HMO. The trap is that out-of-network does not mean free, seamless, or simple. It may mean Original Medicare rules apply, and the beneficiary still has to understand assignment, deductibles, coinsurance, and whether any supplemental coverage is in place.

Why Cost Plans Are Not Just Medicare Advantage By Another Name

Medicare Advantage plans are an alternative to Original Medicare for Part A and Part B coverage, and most include Part D. They may require provider networks, referrals, and prior authorization for certain services. Medicare also notes that Advantage plans have a yearly limit on what you pay for covered Medicare services, while Original Medicare has no yearly out-of-pocket limit unless you have other coverage such as Medigap, Medicaid, employer coverage, retiree coverage, or union coverage .

Cost Plans sit in a different lane. They are included among Medicare health plans, but the 2026 handbook explains that they have some, but not all, of the same rules as Medicare Advantage plans, and that each type has special rules and exceptions . This is not just a technical distinction. It changes the questions a broker should ask. A Medicare Advantage comparison often begins with the network and maximum out-of-pocket exposure. A Cost Plan review has to go further, because the member may be moving between plan rules and Original Medicare rules depending on how and where care is received.

The Prescription Drug Decision Is Where Many Mistakes Begin

The Cost Plan drug decision is unusually important in 2026 because Part D is changing in ways that can affect household cash flow. Medicare states that yearly out-of-pocket costs for covered Part D drugs are capped at $2,100 in 2026, and after that cap is reached, the beneficiary pays no copayment or coinsurance for covered Part D drugs for the rest of the calendar year . Medicare also says the prices for the first 10 drugs negotiated with participating drug companies take effect January 1, 2026, and beneficiaries should contact their plan for how those negotiated prices affect them .

Cost Plans can complicate the Part D choice because a beneficiary may be able to get drug coverage from the Cost Plan if offered, or join a separate Medicare drug plan. Medicare specifically notes that even if the Cost Plan offers Part D, a beneficiary may still choose a separate Medicare drug plan, but drug coverage can only be added or dropped at certain times . That flexibility is valuable only when used correctly. A person taking no medications in October may still need a credible 2026 Part D strategy because a later uncovered period can create late enrollment penalty exposure if there is no creditable prescription drug coverage.

Enrollment Timing Can Be More Flexible But Not Effortless

One distinctive feature of Cost Plans is timing. Medicare says you can join a Medicare Cost Plan any time the plan is accepting new members and you can leave any time and return to Original Medicare . That sounds simple, especially compared with the tight annual windows that control most Medicare Advantage and Part D decisions. The insider caution is that leaving the health plan and fixing the drug coverage are not always the same event.

For 2026 planning, the timing question should be handled like a sequence, not a single switch. If a beneficiary leaves a Cost Plan, what will replace the medical coverage? If they return to Original Medicare, will they seek Medigap, and will underwriting or state specific rules matter? If they had drug coverage through the Cost Plan, when can they add another Part D plan? Medicare separately warns that if someone drops drug coverage and wants to join another Medicare drug plan or Medicare health plan with drug coverage later, they may have to wait for an enrollment period and may owe a late enrollment penalty if they lack creditable drug coverage .

The Medigap Question Needs Careful Handling

A beneficiary should never assume that a Cost Plan, a Supplement, and Part D will coordinate the same way as every other Medicare arrangement. Medigap is designed to fill gaps in Original Medicare, and the handbook explains that Original Medicare beneficiaries may want Medigap if they do not already have coverage such as Medicaid, employer, retiree, or union coverage . But eligibility, timing, and state rules matter, especially outside the first open enrollment period.

This is where a high quality Medicare review differs from a quick premium comparison. The right question is not simply which plan has the lowest monthly cost. It is whether the beneficiary can see the right physicians, whether out-of-network care will flow through Original Medicare, whether prescription costs are capped and forecasted properly under the 2026 Part D rules, and whether any move could make it difficult to obtain or keep Medigap later. Medicare itself notes that 2026 premium amounts, drug costs, and income limits were not available at the time the handbook went to print, which makes current plan specific verification essential before a beneficiary relies on any projection .

Choosing With A Broker Who Reads The Fine Print

Medicare Cost Plans can be a useful middle ground for the right person in the right county. They can also create false confidence when someone assumes flexibility means simplicity. The safest 2026 decision starts with the beneficiary's physicians, hospitals, prescriptions, travel pattern, income related premium exposure, and tolerance for future underwriting risk. Only then should premiums and extra benefits be weighed.

Vista Mutual helps clients slow the decision down enough to see the hidden moving parts. The goal is not to push every person toward the same Medicare structure. It is to protect the client's access, budget, and future options before a plan change becomes difficult to unwind. For peace of mind before choosing a 2026 Medicare Advantage, Supplement, Part D, or Cost Plan strategy, Consult with the Vista Mutual team.