Medicare Plan Compare Quality Signals And Hidden Coverage Tradeoffs In 2026

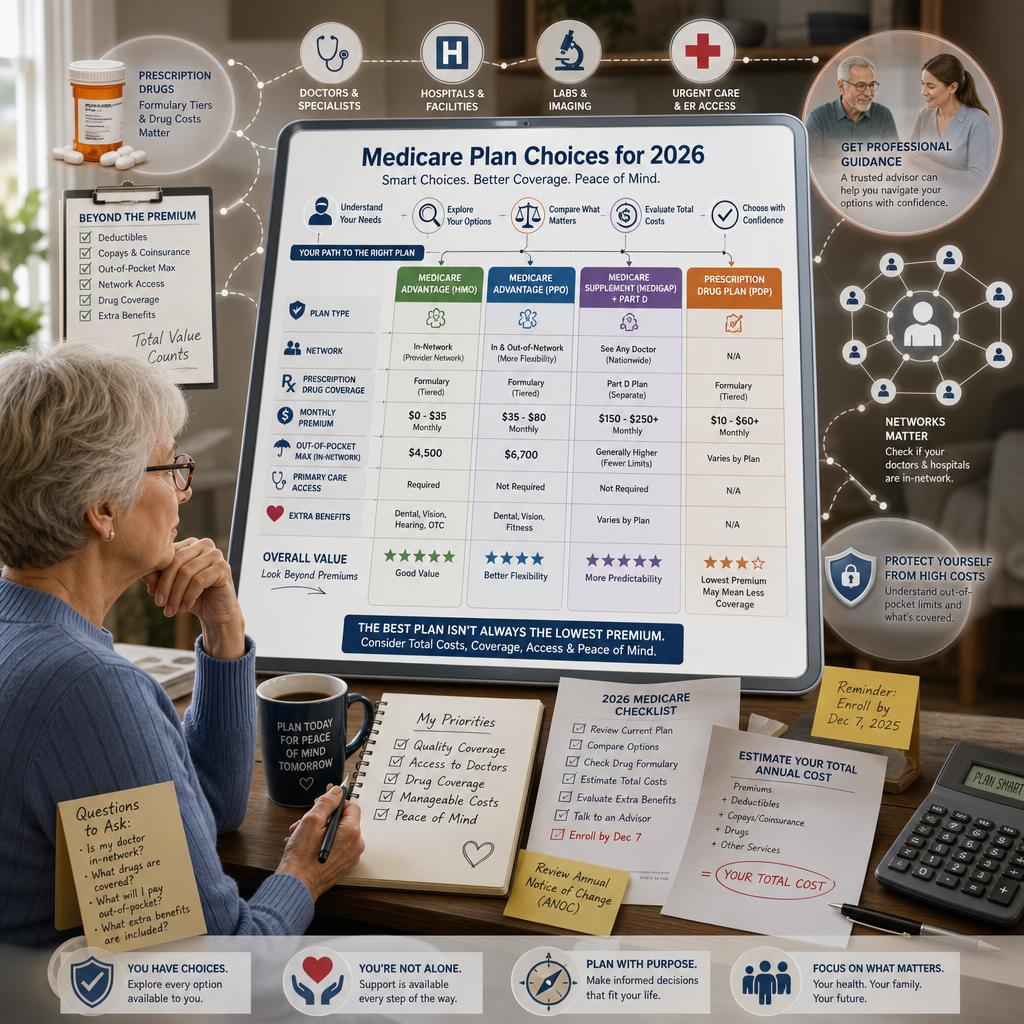

Medicare shoppers often begin with a simple question: Which 2026 plan costs the least each month? It is an understandable instinct, especially for retirees watching fixed income, prescription costs, and household expenses move in different directions. Yet the lowest visible premium is rarely the full Medicare story. In 2026, the more important question is whether a plan can actually perform when your health care becomes complicated.

Consider a beneficiary named Patricia, who takes three maintenance medications, sees a cardiologist twice a year, and wants to keep her preferred hospital. On Medicare.gov, several plans may appear affordable at first glance. But once Patricia looks closer, the decision turns on less obvious factors: whether her cardiologist remains in network, whether her drugs are covered on favorable tiers, whether prior authorization applies, and how much financial protection she has if a serious diagnosis leads to repeated outpatient care.

Why The 2026 Plan Compare Screen Is Only The Starting Point

Medicare encourages beneficiaries to begin comparing 2026 coverage on October 1, 2025, before the October 15 to December 7 Open Enrollment Period. If a change is made, the new coverage begins January 1, 2026, while Medicare Advantage enrollees also have a January 1 to March 31 window to make one Medicare Advantage change or return to Original Medicare with a separate drug plan . Those dates matter because a beneficiary who waits until late December to study networks, formularies, and cost sharing may discover that the most important questions require calls to doctors, pharmacies, and plan representatives.

Plan Compare is useful, but it is not a substitute for professional interpretation. Medicare itself directs beneficiaries to Medicare.gov/plan-compare for plan specific costs and also advises calling plans for details, because the fine print controls what happens at the pharmacy counter, specialist office, and outpatient facility . The 2026 handbook also notes that some premium amounts, drug costs, and income limits were not available at the time of printing, which makes current plan verification especially important before enrolling .

The Quality Question Behind A Low Premium

A Medicare Advantage plan is not merely an insurance card. It is an operating system for care access. The plan decides how networks are built, how referrals work, which services require approval, and how members move through the system when they need specialists, imaging, rehabilitation, or expensive medications. Medicare makes clear that Medicare Advantage plans must cover medically necessary services that Original Medicare covers, but plans may require prior authorization before certain services or supplies are covered .

That difference is where many 2026 mistakes will happen. Original Medicare generally allows beneficiaries to see any Medicare enrolled provider who accepts Medicare patients anywhere in the United States, and in most cases it does not require a referral to use a specialist . Medicare Advantage plans can offer attractive extras, but those extras sit inside a managed plan structure. A plan that looks generous on dental or fitness benefits may still be a poor match if a beneficiary’s oncologist, orthopedic surgeon, infusion center, or preferred hospital is out of network.

Out Of Pocket Protection Is Not The Same In Every Path

One of the most consequential differences between Original Medicare and Medicare Advantage is how financial risk is capped. Original Medicare has no yearly out of pocket limit unless the beneficiary has other coverage, such as Medigap, Medicaid, employer coverage, retiree coverage, or union coverage . Medicare Advantage plans, by contrast, have a yearly limit for covered Part A and Part B services, and once a member reaches that plan limit, the member pays nothing for covered Part A and Part B services for the rest of the year .

That sounds simple, but the practical comparison is not simple at all. A Medicare Advantage plan’s protection depends on its specific in network and out of network rules, its copayments, its coinsurance, and whether the providers you need actually contract with the plan. Original Medicare plus a Medigap policy can reduce exposure to the 20 percent coinsurance that otherwise applies to many Part B services, but Medigap cannot be used to pay Medicare Advantage copayments, deductibles, or premiums . This is why changing from Medigap to Medicare Advantage should be treated as a strategic decision, not a casual annual shopping move.

Drug Costs Look Better In 2026 But The Formulary Still Rules

The most visible 2026 drug change is the Part D out of pocket cap. Medicare states that covered Part D drug costs are capped at $2,100 in 2026, and once that cap is reached, the beneficiary owes no copayment or coinsurance for covered Part D drugs for the rest of the calendar year . This is meaningful protection for people with costly prescriptions, especially those who previously faced unpredictable late year drug expenses.

Still, the cap does not make every Part D or Medicare Advantage prescription drug plan equal. A drug must be covered by the plan, the pharmacy network still matters, and the tier placement can change the beneficiary’s real cost before reaching the cap. Medicare also warns that plans may apply prior authorization, quantity limits, step therapy, opioid safety checks, and drug management programs to certain prescriptions . In plain language, the 2026 cap limits exposure for covered drugs, but it does not eliminate the need to confirm the formulary and restrictions before choosing a plan.

The Annual Notice And Evidence Of Coverage Are Not Optional Reading

The most reliable clues about a 2026 plan often arrive before the sales brochures do. Medicare Advantage plans send an Annual Notice of Change that explains changes in coverage, costs, provider networks, service area, and more for January, while the Evidence of Coverage explains what the plan covers and what the member pays . These documents are not decorative. They are the legal road map for the year ahead.

A beneficiary who ignores these documents may stay in a plan that quietly changes a specialist network, raises a specialist copay, adjusts a drug tier, changes pharmacy arrangements, or modifies extra benefits. The danger is not always dramatic at first. It may appear in February when a drug refill costs more than expected, in April when a prior authorization delays therapy, or in June when a trusted physician is no longer accessible at the expected cost.

How A Professional Review Changes The Decision

A strong 2026 Medicare review should connect the parts of coverage that most people examine separately. The health plan, drug plan, provider network, pharmacy network, prior authorization rules, out of pocket exposure, Medigap rights, and enrollment timing all interact. Medicare even notes that trusted agents and brokers may help beneficiaries compare costs and coverage, alongside resources such as SHIP and Medicare.gov/plan-compare .

This is where Vista Mutual’s role becomes practical. A polished plan summary can show the upside of a plan, but an experienced Medicare brokerage looks for the downside before the client feels it. That means testing the plan against the client’s actual doctors, actual prescriptions, expected procedures, travel habits, chronic conditions, and tolerance for managed care rules. It also means explaining when staying put is wise, when switching is justified, and when a seemingly attractive Medicare Advantage plan could jeopardize future Medigap flexibility.

A Calmer Way To Choose 2026 Medicare Coverage

The best Medicare decision is not always the cheapest, and it is not always the plan with the longest list of extras. It is the plan that holds up under the specific medical life you are likely to live in 2026. For one person, that may mean Original Medicare with a Supplement and a carefully selected Part D plan. For another, it may mean a Medicare Advantage plan with the right doctors, a tolerable authorization process, and a drug formulary that fits.

Medicare has become too consequential to treat as an annual guess. If you want a clear, disciplined review of your 2026 options, Schedule your 2026 Medicare consultation with Vista Mutual. The peace of mind comes from knowing that someone has read beyond the premium and tested the plan against the real world you depend on.