Retiree Union Coverage And Medicare Advantage In 2026 The One Plan Rule Few People Notice

A retired teacher in early 2026 opens a thick benefits packet from her former school district. The headline is reassuring: lower premiums, familiar retiree coverage, prescription drug benefits included. What the headline does not say clearly is that joining one Medicare Advantage plan may affect not only how she receives Medicare, but whether her spouse can keep certain retiree benefits, whether she can use a separate Part D plan, and whether a future move back to Original Medicare will be simple or medically underwritten.

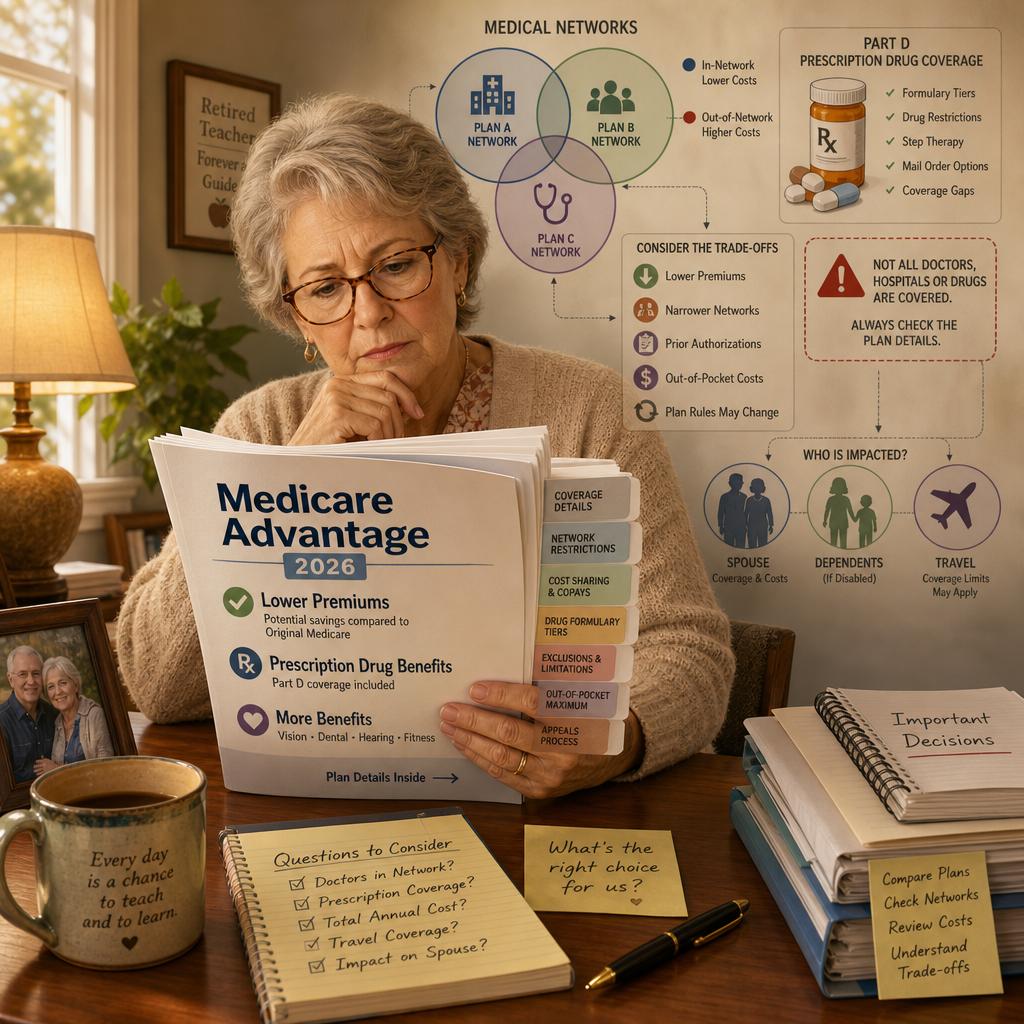

That is the quiet complexity of retiree union and employer Medicare coverage. Many retirees assume their former employer is simply helping pay for Medicare. In reality, some retiree programs are built around group Medicare Advantage contracts, separate drug arrangements, wraparound benefits, or reimbursement accounts. The difference matters because Medicare allows you to be in only one Medicare Advantage plan at a time, and the official 2026 Medicare guidance warns that joining a Medicare Advantage plan can, in some cases, cause you to lose employer or union coverage for yourself, your spouse, and your dependents, sometimes without an easy path back .

The Retiree Plan Is Not Always Just A Supplement

One of the most common misunderstandings Vista Mutual sees is the belief that retiree coverage always works like a Medicare Supplement. It may not. A true Medigap policy helps pay certain out-of-pocket costs under Original Medicare, but it is not the same as a Medicare Advantage plan, and it cannot be used to pay Medicare Advantage copayments, deductibles, or premiums. Medicare’s 2026 handbook is direct on this point: if you are in a Medicare Advantage plan, it is illegal for anyone to sell you a Medigap policy unless you are switching back to Original Medicare .

This distinction becomes especially important when a retiree receives an offer from a former employer that says the plan includes hospital, medical, and drug benefits. That language often describes a Medicare Advantage plan with Part D drug coverage, not a supplement layered on top of Original Medicare. Once enrolled, most Medicare services are covered through the plan rather than paid directly by Original Medicare, and most Medicare Advantage plans include prescription drug coverage . The retiree may still have Medicare, but the operational rules have changed.

The One Plan Rule Can Disrupt A Comfortable Routine

For 2026, the practical issue is not whether a retiree plan is good or bad. It is whether the retiree understands the trade. A group Medicare Advantage plan may offer attractive premiums, extra benefits, and integrated drug coverage. But it may also require the use of a provider network and, for non-emergency care, the plan’s service area. Medicare explains that Medicare Advantage members may need to use doctors and other providers in the plan network and may need referrals for specialists, while Original Medicare generally allows access to any Medicare-enrolled provider who accepts Medicare patients anywhere in the United States .

Consider a retiree who spends winters near adult children in another state. Her former employer’s plan may have strong local hospitals at home, but a narrower out-of-area network where she spends three months each year. If her cardiologist, oncology center, or orthopedic group is not in the network, the plan may not cover non-emergency or non-urgent care outside the rules, or the costs may be higher. Medicare’s 2026 guidance notes that Medicare Advantage costs depend in part on whether services come from a network provider or from someone who does not contract with the plan . That is not a small detail for retirees who travel, split time between states, or maintain longstanding physician relationships.

Drug Coverage Creates A Second Layer Of Risk

The prescription drug side is just as important. Many retiree Medicare Advantage plans include Part D drug coverage. If a retiree joins a different Medicare Advantage plan or a standalone drug plan without confirming the employer’s rules, the former employer may treat that as a voluntary exit from the retiree package. Medicare specifically advises retirees to talk with their employer, union, or benefits administrator before joining a Medicare Advantage plan because the decision may affect coverage for the retiree, spouse, and dependents .

The stakes are higher in 2026 because prescription drug planning is changing. Medicare drug plans will cap yearly out-of-pocket costs for covered Part D drugs at $2,100 in 2026, and once that limit is reached, the beneficiary will not pay a copayment or coinsurance for covered Part D drugs for the rest of the calendar year . That cap is valuable, but it does not make every drug plan interchangeable. Formularies, tiers, preferred pharmacies, mail order rules, prior authorization, and whether a drug is covered at all can still vary by plan. Medicare’s own explanation of 2026 drug costs emphasizes that actual costs depend on prescriptions, formulary placement, tiers, benefit phase, pharmacy choice, and whether the beneficiary receives Extra Help .

The Medigap Exit Question Most Retirees Ask Too Late

A retiree may accept a group Medicare Advantage plan in January and feel satisfied for several years. Then a specialist leaves the network, the retiree develops a condition requiring care at an out-of-state center, or the employer changes vendors. At that moment, the question becomes: can I return to Original Medicare and buy a Medigap policy?

Sometimes the answer is favorable, but not always. Medicare explains that the Medigap Open Enrollment Period generally lasts six months and begins the first month a person has Part B and is 65 or older. After that period, a person may not be able to buy a Medigap policy, or it may cost more, unless a guaranteed issue right or state-specific protection applies . Medicare also warns that if you drop Medigap to join Medicare Advantage, you may not be able to get the same policy back, and in some cases you may not be able to get any Medigap policy unless a trial right or other protection applies .

A Smarter 2026 Review Starts Before Enrollment

The best retiree coverage review is not a premium comparison. It is a systems check. Before enrolling in or leaving an employer or union Medicare option, a retiree should confirm whether the plan is Medicare Advantage, whether Part D is included, whether a separate Part D plan would cancel employer benefits, whether dependents are affected, how the provider network works in every location where care is received, and what rights exist if the retiree later wants Original Medicare with a Medigap policy.

This is where professional guidance changes the emotional experience of Medicare. Instead of hoping the retiree packet means what it appears to mean, you can have the moving parts translated into plain English: plan type, drug structure, network exposure, spouse impact, Medigap consequences, and 2026 cost protections. Vista Mutual Insurance Services helps clients compare Medicare Advantage, Supplements, and Part D choices with the kind of caution retiree benefits deserve. For a careful review before you enroll, leave, or replace retiree coverage, Schedule your 2026 Medicare consultation.