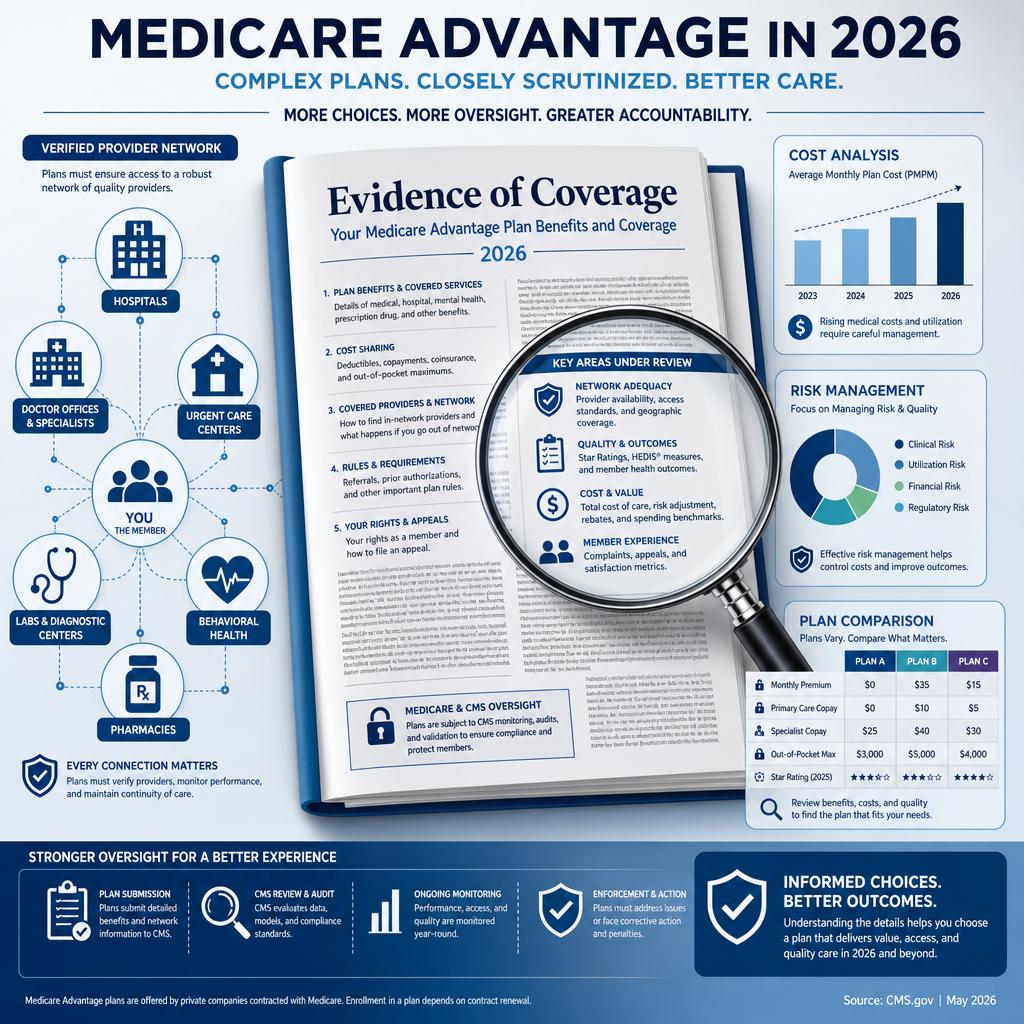

The 2026 Medicare Advantage Evidence Of Coverage Audit

A Medicare Advantage plan is often chosen in a moment of optimism. The premium looks manageable, the dental allowance sounds helpful, the pharmacy appears familiar, and the summary chart seems to promise a simpler way to receive care. Yet in 2026, the most important document is not the sales brochure. It is the Evidence of Coverage, the contract-style guide that explains how the plan actually pays, restricts, approves, and coordinates benefits.

For many beneficiaries, the difference only becomes clear after a medical event. A retired teacher may discover that her orthopedic surgeon is in network, but the outpatient facility he uses is not. A widower with heart disease may learn that a diagnostic test requires prior authorization even though his doctor ordered it urgently. A couple may choose a plan for a dental benefit, then find that the covered procedures, provider rules, annual allowance, and claim process are narrower than expected. These are not small technicalities. They are the mechanics of how Medicare Advantage works.

Why The Evidence Of Coverage Matters More In 2026

Medicare’s own materials make clear that the Evidence of Coverage gives details about what a plan covers, how much you pay, and more, while the Annual Notice of Change identifies changes in costs, coverage, provider networks, service area, and related rules for the coming January . The Annual Notice of Change tells you what changed. The Evidence of Coverage tells you what you are agreeing to live under.

That distinction matters because Medicare Advantage is not simply Original Medicare with extras attached. It is an alternative way to receive Part A and Part B benefits through a private plan approved by Medicare. Plans must cover medically necessary services that Original Medicare covers, but they may use networks, different cost sharing, prior authorization, and plan-specific administrative procedures . In practice, two plans with similar premiums can operate very differently when a beneficiary needs specialist care, post-hospital services, chemotherapy, imaging, or durable medical equipment.

The Cost Story Is Bigger Than The Premium

A low or even zero-dollar Medicare Advantage premium can be attractive, but it is only one part of the financial picture. Medicare explains that Medicare Advantage costs depend on whether the plan charges a premium, whether it helps pay part of the Part B premium, whether there are deductibles, what copayments or coinsurance apply, whether care is in network, and how often services are needed . That means the plan that looks inexpensive in January may be more costly in July if your doctors, facilities, drugs, and therapy needs do not align with the plan’s structure.

The larger planning issue is the difference between predictable and conditional costs. Original Medicare generally charges 20 percent of the Medicare-approved amount for Part B-covered services after the deductible, and there is no yearly out-of-pocket limit unless you have supplemental coverage such as Medigap, Medicaid, employer coverage, retiree coverage, or union coverage . Medicare Advantage plans, by contrast, have a yearly limit on what you pay for covered Medicare services, but the protection comes with plan rules, network expectations, and possible prior authorization requirements . The Evidence of Coverage is where those tradeoffs become visible.

The Fine Print That Changes A Real Medical Bill

A serious plan review in 2026 should not begin with the premium. It should begin with the medical life of the person enrolling. Does the beneficiary use a specific cancer center, cardiology group, infusion site, orthopedic practice, home health agency, or skilled nursing facility? Does the plan require referrals? Are out-of-network services covered at all for non-emergency care? If they are covered, does the plan impose higher cost sharing or separate limits? Medicare notes that Medicare Advantage enrollees may need to use providers in the plan’s network and service area for non-emergency care, and some plans cover non-emergency out-of-network care only at a higher cost .

This is where beneficiaries often mistake access for coverage. A doctor’s office may say, “We take Medicare,” but that does not always mean the office participates in a specific Medicare Advantage network. A hospital may be in network, while an anesthesiology group, imaging location, or rehabilitation provider may not be. The Evidence of Coverage will not replace a live provider directory check, but it tells you how the plan treats network status, referrals, emergency care, urgently needed care, and out-of-area services.

Prior Authorization Is Not Just A Plan Annoyance

Prior authorization can affect the timing and location of care. Medicare explains that, unlike Original Medicare in most cases, Medicare Advantage plans may require approval before covering certain services or supplies . That does not mean the plan will deny care. It means the plan can require a formal review before payment, and the beneficiary needs to understand how that review works before a health crisis creates urgency.

The Evidence of Coverage often explains when an organization determination can be requested. Medicare describes this as a decision from the plan, spoken or in writing, that tells whether a service, drug, or supply is covered and how much the beneficiary may have to pay . This is insider-level practical value: before an elective procedure, expensive medication, home health episode, or specialized equipment order, a written determination can be far more useful than a reassuring phone conversation that cannot be reproduced later.

Prescription Drugs Add Another Layer In 2026

Drug coverage deserves its own reading of the Evidence of Coverage and formulary, especially because 2026 includes major Part D changes. Medicare states that out-of-pocket costs for covered Part D drugs are capped at $2,100 in 2026, and once that threshold is reached, beneficiaries pay no copayment or coinsurance for covered Part D drugs for the rest of the calendar year . That is a meaningful protection, but it does not make every plan interchangeable.

The plan still controls which covered drugs are on the formulary, what tier they occupy, which pharmacies provide preferred pricing, and whether utilization rules apply. Medicare also notes that negotiated prices for the first 10 selected drugs take effect January 1, 2026, and beneficiaries should contact their plan for details about how those prices affect them . A beneficiary taking several medications should not assume that the $2,100 cap alone identifies the best plan. The route to that cap, the monthly cash flow, the pharmacy arrangement, and the plan’s formulary rules still matter.

A Professional Audit Looks For Friction Before It Becomes A Denial

A high-quality 2026 Medicare review reads the Evidence of Coverage like a risk map. The goal is not to frighten people away from Medicare Advantage. For many beneficiaries, the right plan can offer coordinated care, predictable copays, drug coverage, and valuable supplemental benefits. The goal is to understand whether the plan’s rules match the beneficiary’s physicians, diagnoses, medications, travel habits, budget, and tolerance for administrative friction.

One disciplined review should confirm the plan’s service area, primary care rules, specialist access, referral requirements, prior authorization categories, inpatient and outpatient cost sharing, drug formulary placement, preferred pharmacies, supplemental benefit limits, emergency and urgent care rules, and the annual maximum out-of-pocket protection. That is the only list this article needs, because every item on it can become a real claim issue if ignored.

The most expensive Medicare mistake is often not choosing a “bad” plan. It is choosing a plan that was never built for your actual life. A person with few doctors and low medication needs may value a different structure than someone managing cancer therapy, complex diabetes, mobility equipment, or multi-specialist cardiac care. A snowbird, a caregiver spouse, and a retiree who wants access to a particular academic medical center may each need a different answer.

Medicare planning in 2026 is no longer a matter of comparing premiums in a chart. It is contract interpretation, provider verification, drug analysis, and risk management. Vista Mutual helps clients look past the brochure and understand how Medicare Advantage, Medicare Supplements, and Part D plans behave when care becomes real. For confidence before you enroll, renew, or switch, Schedule your 2026 Medicare consultation with the Vista Mutual team.