The 2026 Medicare Part D Explanation Of Benefits Audit

In 2026, many Medicare beneficiaries will hear the headline number first: covered Part D drug costs are capped at $2,100 for the year. That is a meaningful protection, but it can also create a false sense of simplicity. The cap does not mean every prescription is automatically protected, every pharmacy transaction counts the same way, or every plan will process your medications without friction. Medicare’s own 2026 handbook confirms that the $2,100 cap applies to yearly out-of-pocket costs for drugs covered by your Part D plan, and once you reach that cap, you pay no copayment or coinsurance for covered Part D drugs for the rest of the calendar year .

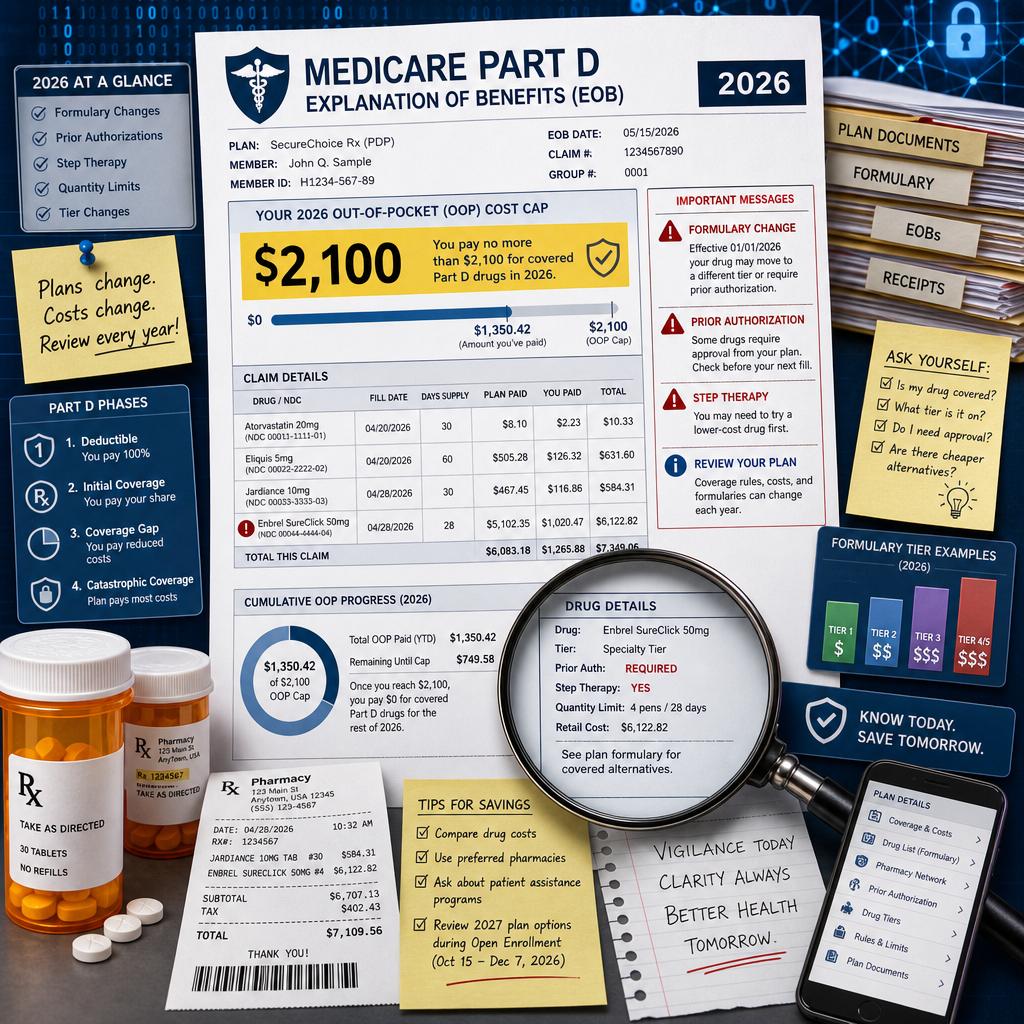

The document that quietly tells the story is the Part D Explanation of Benefits, often called the EOB. It arrives after you fill prescriptions, and many people treat it like junk mail because it is not a bill. That is understandable, but in 2026 it is also risky. The EOB is where the plan’s version of your drug year becomes visible: which medications were covered, which pharmacy prices were applied, whether a drug was subject to restrictions, and whether your spending is moving toward the $2,100 threshold as expected.

Why The 2026 Part D EOB Matters More Than The Pharmacy Receipt

A pharmacy receipt tells you what happened at the counter. The Explanation of Benefits tells you how the plan interpreted what happened. Those are not always the same thing. A beneficiary may leave the pharmacy relieved that a medication was filled, only to discover later that the claim was processed under a temporary supply, a non-preferred pharmacy arrangement, a formulary exception, or a coverage rule that will matter the next time the prescription is due.

Medicare states that each month you fill a prescription, your plan sends an Explanation of Benefits notice, and beneficiaries are told to review it for mistakes and contact the plan with questions or errors . That instruction is more important in 2026 because the EOB is one of the few practical ways to monitor whether your covered Part D costs are being credited correctly toward the annual cap. A single misclassified medication may not look dramatic in January, but by August it can change whether a beneficiary reaches the cap when expected.

The Covered Drug Question Hidden Inside The 2100 Cap

The phrase “covered Part D drugs” deserves careful attention. If a medication is not on the plan’s formulary, is excluded from Part D, or is paid outside the plan through a discount arrangement that does not process as a covered claim, the transaction may not behave the way a beneficiary assumes. Medicare notes that people may sometimes pay for a drug without insurance, such as through pharmacy savings programs or manufacturer discounts, and should ask the pharmacist whether a less expensive option is available . That can be a reasonable cash-saving decision, but it should be made deliberately, not by accident.

Consider a retiree taking four medications, one of which becomes expensive in the spring. At the pharmacy, a coupon lowers the price below the plan copay, so the beneficiary pays cash and leaves satisfied. The problem is not the coupon itself. The problem is that a cash transaction may not build the same Part D spending record as a covered plan claim. In a year when the cap matters, the cheapest counter price today may or may not be the best annual strategy. This is where a brokerage review becomes practical rather than theoretical, because the right answer depends on the drug, the plan, the pharmacy, the timing, and the beneficiary’s full medication profile.

Formulary Changes Can Turn A Quiet Notice Into An Early Warning

Many beneficiaries assume that once a medication is covered in January, the plan’s treatment of that drug will remain stable all year. That is not always how Part D works. Medicare’s 2026 handbook explains that plans can change their formularies at any time and may notify beneficiaries of formulary changes that affect drugs they take . The EOB may be one of the first places a careful reader notices that something is shifting.

This is especially important for people on brand-name medications, specialty drugs, inhalers, injectables, anticoagulants, oncology therapies, or drugs with limited therapeutic substitutes. A change in tier, utilization management, pharmacy status, or plan messaging can affect the next refill. The mistake many families make is waiting until the refill is denied or delayed. A more disciplined approach is to use the EOB as a monthly audit trail and treat unfamiliar language as a prompt to ask questions before the medication cabinet is nearly empty.

Prior Authorization And Step Therapy Do Not Disappear Because A Cap Exists

The $2,100 cap limits out-of-pocket spending for covered Part D drugs, but it does not erase the plan’s coverage rules. Medicare explains that Part D plans may apply prior authorization, quantity limits, step therapy, opioid safety checks, and drug management programs to certain medications . These rules can determine whether a drug is covered, how much can be dispensed, and what documentation the prescriber must provide.

This is one of the most misunderstood parts of 2026 planning. A beneficiary may reasonably think, “My drug costs are capped, so I no longer need to worry about the details.” In reality, the cap answers only one question: what happens after covered out-of-pocket Part D spending reaches the annual limit. It does not answer whether the drug is on the formulary, whether the prescribed dosage is within plan limits, whether the pharmacy is preferred, whether the prescriber’s documentation is sufficient, or whether the plan requires a lower-cost alternative first.

Reading The EOB Like A Medicare Professional

A professional review starts with pattern recognition. The first EOB of the year establishes the baseline: the medications, pharmacies, tiers, restrictions, and amounts being credited. Later notices should be compared against that baseline. If a medication suddenly appears differently, if a refill cost changes without an obvious reason, if a drug is missing from the notice, or if the EOB suggests a coverage rule is involved, the issue should be clarified quickly.

The most important EOB questions are straightforward: Was the drug processed through the Part D plan, was it treated as covered, was the pharmacy pricing expected, was any utilization management applied, and does the year-to-date spending progress make sense against the $2,100 cap? That is the only list a beneficiary truly needs, but answering those questions can require experience. The plan document, pharmacy system, prescriber’s office, and Medicare rules do not always speak the same language.

How This Affects Medicare Advantage And Standalone Part D Choices

The EOB audit matters whether drug coverage comes through a standalone Part D plan paired with Original Medicare or through a Medicare Advantage plan that includes drug coverage. Medicare explains that most Medicare Advantage plans include Part D, while beneficiaries in Original Medicare can add drug coverage by joining a separate Medicare drug plan . The structure is different, but the risk is similar: the plan’s formulary and pharmacy rules shape the beneficiary’s real experience.

This is also where annual plan selection becomes more nuanced than comparing premiums. A low-premium plan may look attractive until a key drug is restricted, a preferred pharmacy is inconvenient, or a medication is placed on a tier that accelerates early-year costs. Conversely, a plan with a higher premium may still be the better annual value if it handles a beneficiary’s drugs more predictably. The right analysis must include total expected cost, pharmacy access, formulary status, prior authorization exposure, and the likelihood of reaching the cap.

In 2026, the Part D EOB is no longer a passive notice. It is a monthly record of whether your drug plan is performing the way you thought it would when you enrolled. The $2,100 cap is valuable, but it works best when beneficiaries understand what counts, what does not, and what warning signs deserve action before a refill becomes urgent.

Vista Mutual helps clients turn those moving parts into a clear Medicare strategy. If you want a professional review of your 2026 drug coverage, Medicare Advantage options, Supplement fit, and Part D risk points, Schedule your 2026 Medicare consultation with the Vista Mutual team and move into the year with fewer surprises.