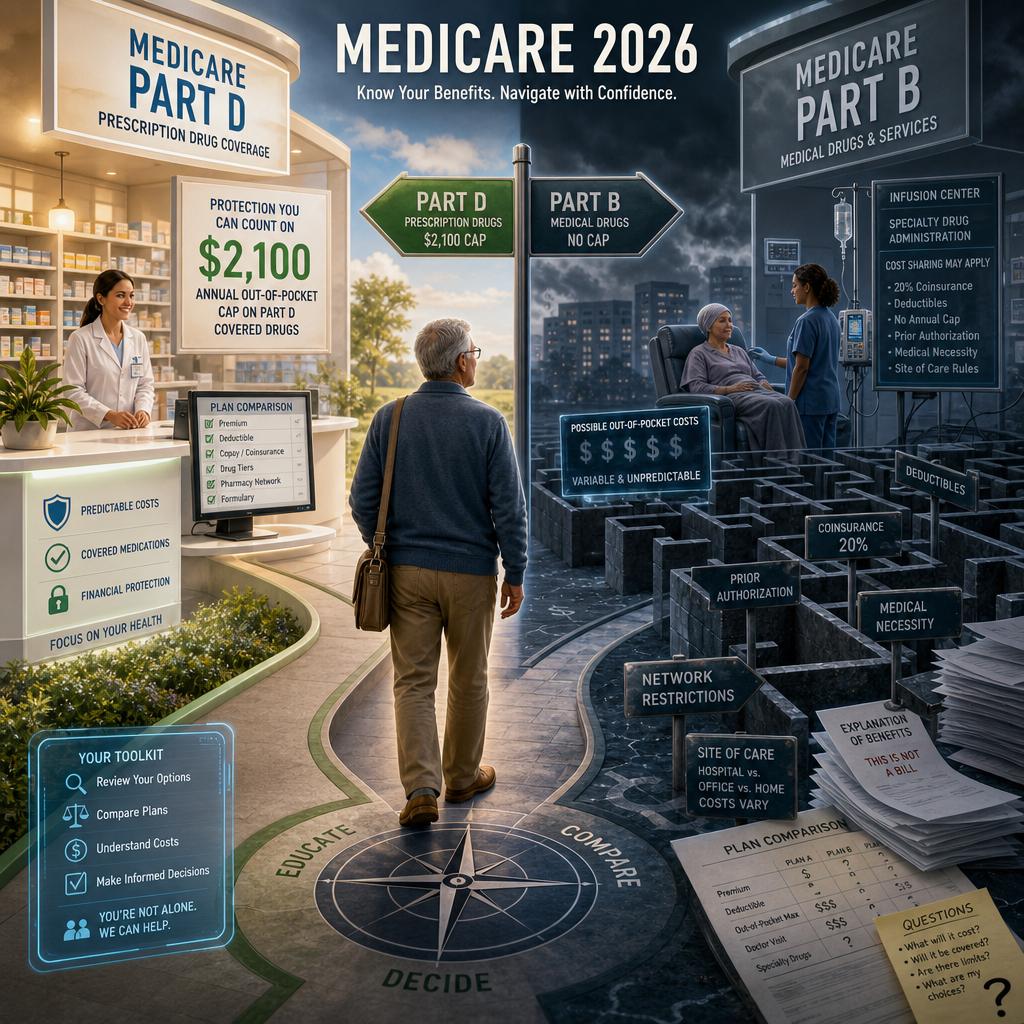

The Part B Drug Blind Spot In 2026 Medicare Planning

A retiree walks into a 2026 Medicare review with understandable confidence. Her prescriptions look manageable, she has heard that Medicare drug coverage now caps yearly out-of-pocket Part D costs at $2,100, and she assumes the biggest medication risk has been contained. Then her rheumatologist recommends an infused biologic, or her oncologist changes a therapy from a pharmacy-filled pill to a clinic-administered drug. Suddenly, the word drug no longer means one thing under Medicare.

That is the Part B drug blind spot. In 2026, the difference between a medication covered by Part D and a medication billed under Part B can determine whether a person is protected by the $2,100 Part D cap or exposed to medical benefit cost sharing. For many households, this is not an academic distinction. It is the difference between choosing a plan based on a formulary and choosing a plan based on how care is actually delivered.

The 2100 Cap Is Real But It Has Borders

The 2026 Medicare handbook is clear that people with Medicare drug coverage have a yearly out-of-pocket cap of $2,100 for covered Part D drugs, and once that cap is reached, they pay no copayment or coinsurance for covered Part D drugs for the rest of the calendar year . That is an important consumer protection, especially for people taking costly brand name medications, specialty drugs, or drugs affected by tier placement. It also changes how beneficiaries should evaluate premiums, deductibles, pharmacy networks, and the timing of refills.

But the protection is not universal. The cap applies to covered drugs under a Part D plan, not to every medication that a physician may prescribe or administer. Medicare itself warns that actual drug costs vary based on whether a medication is on the plan formulary, which tier it falls into, which pharmacy is used, whether the person has Extra Help, and which benefit phase applies . The hidden issue is that some of the most expensive therapies may never enter that Part D cost pathway at all.

Why Some Medications Live Under Part B

Medicare Part B does not cover most drugs, but it does cover certain exceptions, including some infused and injected drugs given in a doctor’s office, insulin used with a traditional pump, immunosuppressive drugs, and medications used for hospice pain and symptom management . In practical terms, that means the same person can have ordinary retail prescriptions processed at the pharmacy under Part D while other therapies are billed as medical services under Part B.

This is where many plan comparisons become dangerously shallow. A beneficiary may enter a medication list into a drug plan search tool and receive a clean-looking estimate, only to discover later that an infusion center, oncology practice, dialysis related therapy, or pump supplied medication is handled through the medical side of Medicare. The route of administration, the setting of care, the diagnosis, and even who supplies the medication can matter as much as the drug name itself.

Original Medicare And The Cost Sharing Problem

Under Original Medicare, Part B services generally work through a deductible and coinsurance structure. The 2026 Medicare handbook explains that after the Part B deductible is met, Medicare usually pays its share and the beneficiary typically pays 20 percent of the Medicare-approved amount when the provider accepts assignment . For a routine office visit, that may feel manageable. For a high-cost medication administered in a clinical setting, 20 percent can become a much more serious number.

There is another layer of risk. Original Medicare does not have a yearly out-of-pocket maximum unless a person has other coverage, such as Medigap, Medicaid, employer coverage, retiree coverage, or union coverage . That is why a beneficiary who expects ongoing Part B drug therapy may need to evaluate Medicare Supplement options differently than a person whose medication exposure is almost entirely retail pharmacy based.

Medicare Advantage Changes The Math But Adds Conditions

Medicare Advantage plans must cover medically necessary services that Original Medicare covers, and many plans include Part D coverage as part of the same package. They also have a yearly limit on what members pay for covered Medicare services, after which the member pays nothing for covered services for the rest of the year . That out-of-pocket limit can be valuable when costly Part B services are expected.

Yet Medicare Advantage is not simply Original Medicare with a ceiling added. Plans may require network providers, may use different cost sharing for services, and may require prior authorization before covering certain services or supplies . A beneficiary receiving Part B drugs should not only ask whether the medication is covered. The more precise questions are whether the prescribing specialist is in network, whether the infusion location is contracted, whether prior authorization is likely, and how the plan classifies the therapy for cost sharing.

The 2026 Review That Most Shoppers Skip

A serious 2026 Medicare review should separate medications into pharmacy drugs and medical benefit drugs. This cannot be done by name alone. A careful advisor asks where the drug is received, who administers it, whether it is self-administered, whether it is supplied by a pharmacy, physician office, durable medical equipment supplier, or infusion provider, and whether the therapy is tied to a diagnosis that changes the billing pathway.

The Medicare Prescription Payment Plan adds another wrinkle. It can help spread out-of-pocket costs for covered Part D drugs across the calendar year, but Medicare states that it does not save money or lower drug costs . Just as important, it is a Part D payment option. It should not be mistaken for protection against every medical bill connected to a medication.

The policy environment is also shifting. Medicare notes that negotiated prices for the first 10 selected drugs take effect on January 1, 2026, and beneficiaries should contact their plans to understand how those negotiated prices affect them . That makes 2026 a year when assumptions based on last year’s drug costs may be especially unreliable.

The Peace Of Mind Comes From Mapping The Whole System

The lesson is not that one Medicare path is always better. It is that the right answer depends on the whole architecture of care. A low premium Part D plan may be reasonable for one person and inadequate for another. A Medicare Advantage plan with a medical out-of-pocket limit may look attractive, but only if the physicians, facilities, and authorization rules fit the person’s real treatment pattern. Original Medicare with a Supplement may offer broader provider access, but the timing and availability of Medigap rights can be consequential.

Vista Mutual Insurance Services helps clients look beneath the surface of the brochure, where the real financial exposure often sits. If you take specialty medications, receive injections or infusions, use a pump, see multiple specialists, or simply want your 2026 Medicare decision reviewed with clinical and policy precision, Schedule your 2026 Medicare consultation. Professional guidance turns a confusing set of rules into a plan you can live with, with fewer surprises and far more confidence.